X++ programming blog series

Further reading:

Import a D365 FO entity with a virtual KEY field

Print a custom product label: a Template solution in Process Guide Framework, with detours

Extending SysOperation contracts with DataMemberAttribute

X++ Decorator pattern in Dynamics 365

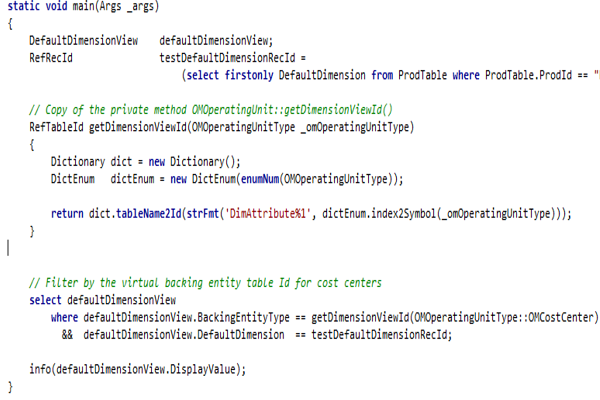

Get a cost center in D365FO

Find and merge a DimensionAttributeValue

SysExtension framework pitfall: avoid new()

Input validation and messaging in the Process Guide Framework